Patent Expiry and Unregulated Compound Proliferation: A Weak Signal Reshaping the Diet Drug Ecosystem

Patent expirations paired with regulatory challenges around compounded GLP-1 drugs suggest a nascent disruption in the diet drug sector that could redefine capital flows, market access, and regulatory control over the next decade.

The imminent patent expiry of semaglutide-based GLP-1 (glucagon-like peptide-1) drugs in multiple emerging and developed markets introduces a subtle but structurally significant inflection for obesity pharmacotherapy. Alongside, the surge of non-FDA-approved compounded formulations sold predominantly via telehealth platforms challenges existing regulatory frameworks and industry structures. This dual development—often viewed in isolation either as a simple patent cliff or enforcement issue—may synergistically drive a fragmented, multi-tier system of diet drug access and innovation. Understanding this emerging signal is critical for senior leaders shaping pharmaceutical capital deployment, regulatory modernization, and competitive strategy over the next 5 to 20 years.

Signal Identification

This development qualifies primarily as an emerging inflection point with weak signal characteristics. While patent expirations are routine, the simultaneous escalation in unregulated compound drug marketing and variable enforcement introduces systemic ambiguity unprecedented in obesity pharmacotherapy. It is not yet widely recognised how this confluence could destabilize incumbent innovators’ control and regulatory governance. The time horizon is medium term (5–10 years) with a medium to high plausibility band given global patent schedules and regulatory enforcement trends. Sectors most exposed include pharmaceuticals, telehealth, regulatory bodies, healthcare payors, and digital health platforms.

What Is Changing

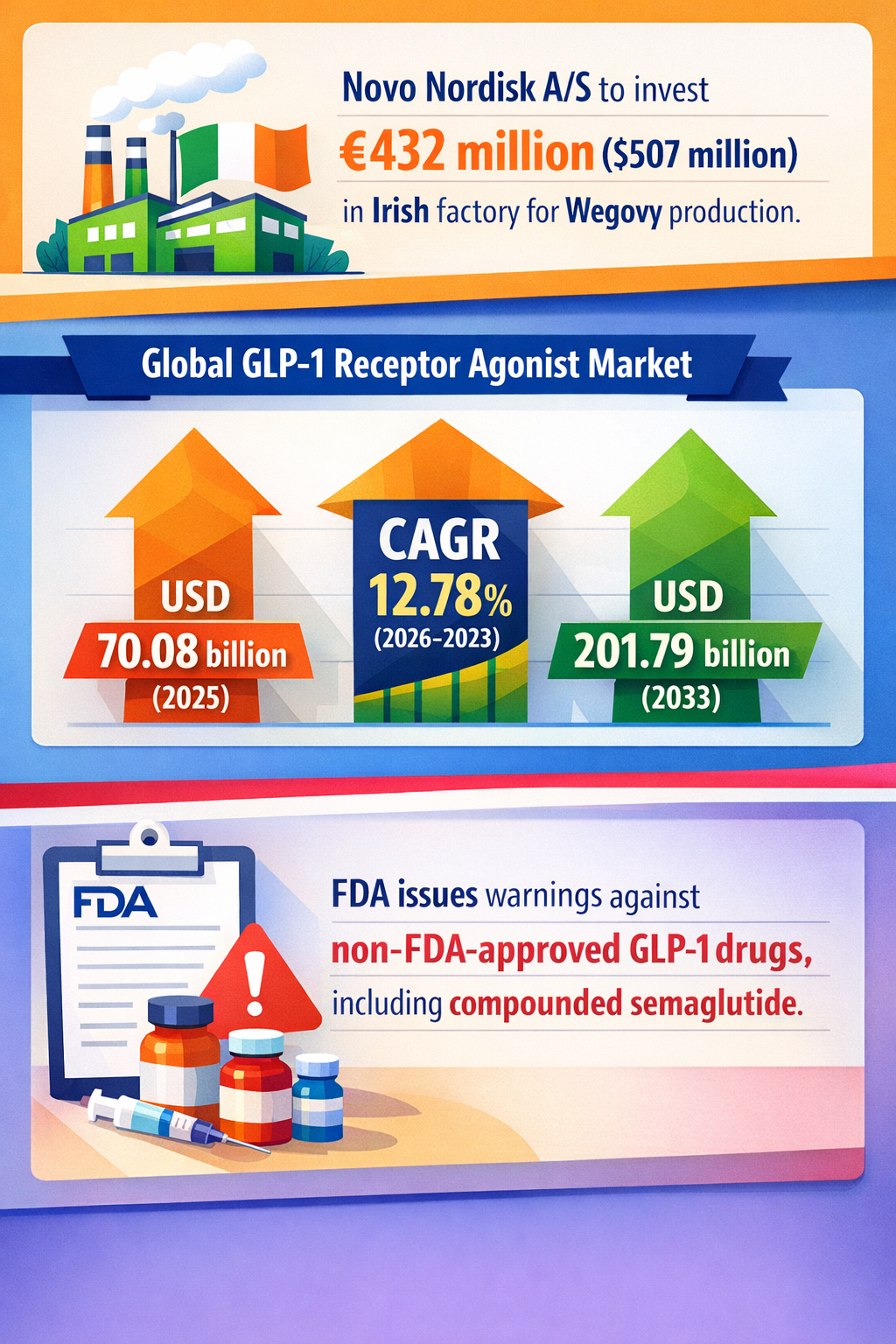

The patent protection for the GLP-1 drug semaglutide is expiring imminently in key markets such as Brazil, China, India, and across over 150 other countries where patents never existed (ScienceAlert 07/03/2026). This creates a rare global window for low-cost generics or biosimilars to enter mass markets, potentially slashing prices dramatically from current branded levels. Novo Nordisk's announcement to cut list prices by nearly 50% in 2027 signals anticipation of this erosion (Slepko Law 19/03/2026).

Concurrently, an unregulated “grey market” of compounded GLP-1 drugs is expanding rapidly, heavily marketed on telehealth platforms like Hims & Hers, often implying FDA approval where none exists (People’s Pharmacy 13/03/2026). Such compounds contain impurity risks and suffer quality variability, as seen with tirzepatide formulations containing vitamin B12 impurities (KFF Health News 13/03/2026). The FDA is aggressively issuing warning letters and considering enforcement actions, but persistent sales via online and telehealth channels complicate regulation (Debrunner US 12/02/2026).

These concurrent moves suggest an evolving two-tier access dynamic: an established branded pharmaceutical ecosystem hedging against generic erosion, and a parallel telehealth-driven channel operating in regulatory grey zones. The structural novelty lies in the interaction between patent expiry's democratizing force and regulatory friction around compounded drugs, neither of which alone fully account for systemic reconfiguration.

Disruption Pathway

This dual development could escalate under several accelerating conditions. First, falling prices post-patent expiry may incentivize broad adoption of generics in emerging markets, redirecting capital from incumbent pharmaceutical pipelines to local or telehealth-based production and distribution models. Second, persistent demand-side pressures (e.g., rising obesity rates and expanded Medicare coverage) drive consumers to seek lower-cost alternatives regardless of regulatory status.

These conditions stress conventional regulatory oversight mechanisms, which traditionally rely on brick-and-mortar prescribing and supply chains. The rise of telehealth-specific marketing and direct-to-consumer compounded drugs outpaces regulatory enforcement capacities, producing enforcement bottlenecks and compliance gaps. To adapt, regulators may either tighten digital oversight frameworks or create new approval pathways for compounded or biosimilar products.

This regulatory flux could catalyse structural adaptation within pharmaceutical supply chains through vertical integration of compounding pharmacies, technology-enabled quality assurance platforms, or franchise models blending telehealth providers and local manufacturing. In turn, these adaptations reinforce new consumer access patterns via cash-pay channels, reshaping payer strategies, notably within Medicare and private insurance markets.

Feedback loops emerge as incumbents face profit margin pressures, incentivizing more aggressive branded price cuts or collaborative agreements with telehealth platforms, as seen in Novo Nordisk’s collaboration with Hims (WRAL 05/02/2026). Conversely, public safety concerns linked to compound quality may provoke liability risks and stricter regulatory scrutiny, accelerating industry consolidation or public-private partnerships for quality assurance.

Eventually, dominant models for drug approval, distribution, and payment may realign toward hybrid frameworks that formally integrate telehealth-enabled compounding, biosimilar generics, and digital pharmacovigilance, diverging from the exclusive patented-brand centric model predominant in recent decades.

Why This Matters

This signal is vital for decision-makers steering capital deployment in pharma R&D, manufacturing, and digital health. Investors may need to recalibrate valuations of branded obesity drug developers in light of downward pricing pressure and fragmented market entry. Regulators face the complex mandate to safeguard efficacy and safety across hybrid supply chains without stifling increased access triggered by generics and compounding.

Competitive positioning will shift toward players able to navigate multi-channel market access strategies combining traditional brand equity with telehealth partnerships or biosimilar development. Supply chains will likely become more distributed, putting a premium on supply chain transparency and digital quality controls.

Governments and insurers must weigh expanding coverage policies, such as Medicare drug price negotiation effectiveness, alongside the risk of unregulated compounding proliferation to avoid parallel black markets undermining public health goals. Liability frameworks will also be tested as adverse events potentially linked to non-standardized compounded drugs attract scrutiny.

Implications

The emergence of a hybrid diet drug ecosystem combining expiry-driven generics and digitally marketed compounded drugs may structurally lower treatment costs while simultaneously fragmenting quality control and regulatory scope. This could democratize obesity pharmacotherapy access globally but introduces new layers of regulatory complexity and liability risk.

This is likely a structural shift rather than transient noise, as patent cliffs are predictable but their interaction with telehealth-driven compounding enforcement gaps is still underappreciated. It could catalyse more inclusive yet riskier obesity treatment markets, requiring recalibrated regulatory frameworks and investment in digital pharmacovigilance.

The development is not merely a pricing war or temporary counterfeit surge but an inflection in pharmaceutical industrial structure and regulatory governance. Alternative interpretations might view compounded drug proliferation as a purely illegal or minor outlier risk; however, the scale and coordination observed suggest it could become a normalized access route if unchecked.

Early Indicators to Monitor

- Regulatory policy drafts or guidelines addressing telehealth-compounded GLP-1 drug oversight

- Venture funding directed to digital pharmacovigilance and quality assurance solutions for compounded meds

- Patent litigation outcomes and generic drug approvals in emerging markets

- Capital reallocation trends within pharmaceutical companies toward biosimilar development

- Enforcement volume and legal action frequency targeting telehealth compounding networks

Disconfirming Signals

- Effective and swift regulatory enforcement shutting down non-FDA-approved compounded GLP-1 products completely

- Slower-than-expected uptake of generic semaglutide options in key markets due to manufacturing or distribution barriers

- Incumbent pharmaceutical firms maintaining dominant market share through successful patent extensions or exclusive contracts with payors

- Absence of telehealth platform adoption or consumer resistance to compounded drug offerings

Strategic Questions

- How should pharmaceutical manufacturers realign R&D and pricing strategies anticipating a two-tier market combining generics and compounded drugs?

- What regulatory frameworks or public-private collaborations could best mitigate safety risks without constraining equitable access?

Keywords

GLP-1; semaglutide; patent expiry; compounded drugs; telehealth; obesity pharmacotherapy; regulatory enforcement; biosimilars; drug pricing; pharmaceutical industrial structure

Bibliography

- Weight loss drugs could cost just $3 a month to make as patents end. ScienceAlert. Published 07/03/2026.

- Novo Nordisk has announced that it intends to cut Ozempic and Wegovy list prices nearly 50% commencing in 2027. Slepko Law. Published 19/03/2026.

- More than one-third of telehealth sites marketing compounded GLP-1 drugs suggested or implied FDA approval, and many failed to clearly reveal risks or side effects. People’s Pharmacy. Published 13/03/2026.

- FiercePharma: Lilly Warns Of Impurity In Some Compounded Tirzepatide Drugs. KFF Health News. Published 13/03/2026.

- The FDA announced that it will take enforcement action against non-FDA-approved GLP-1 active pharmaceutical ingredients. Debrunner US. Published 12/02/2026.

- Hims will stop advertising compounded GLP-1 drugs on its platform or in its marketing. WRAL. Published 05/02/2026.